The Cost of NOT Owning Your Home

Owning a home has great financial benefits, yet many continue to rent! Today, let’s look at the financial reasons why owning a home of your own has been a part of the American Dream for as long as America has existed.

Zillow recently reported that:

“In reality, buying or renting a home is an intensely personal decision, with emotional and even financial considerations that go beyond whether to invest in this one (admittedly large) asset. Looking strictly at housing market numbers, there is a concrete point at which buying a home makes more financial sense than renting it.”

What proof exists that owning is financially better than renting?

1. We recently highlighted the top 5 financial benefits of homeownership:

- Homeownership is a form of forced savings.

- Homeownership provides tax savings.

- Homeownership allows you to lock in your monthly housing cost.

- Buying a home is cheaper than renting.

- No other investment lets you live inside of it.

2. Studies have shown that a homeowner’s net worth is 44x greater than that of a renter.

3. Just a few months ago, we explained that a family that purchased an average-priced home at the beginning of 2017 could build more than $48,000 in family wealth over the next five years.

4. Some argue that renting eliminates the cost of taxes and home repairs, but every potential renter must realize that all the expenses the landlord incurs are already baked into the rent payment– along with a profit margin!!

Bottom Line

Owning a home has always been, and will always be, better from a financial standpoint than renting.

What does this mean for you?

Call us at (850) 420-7200 or contact us if you're ready to explore the possibility of owning your home and we'll evaluate your situation to determine the best fit for you.

Existing Home Sales Slowed by a Lack of Listings

Some Highlights:

- The inventory of existing homes for sale has dropped year-over-year for the last 29 consecutive months and is now at a 3.9-month supply.

- Existing home sales are currently at an annual pace of 5.48 million, the highest pace since June of this year, but down 0.9% from October 2016.

- NAR’s Chief Economist, Lawrence Yun, had this to say: “While the housing market gained a little more momentum last month, sales are still below year ago levels because low inventory is limiting choices for prospective buyers and keeping price growth elevated.”

What does this mean for you?

Call us at (850) 420-7200 or contact us, even if you're not quite ready to sell, and we'll share more important info that applies directly to you.

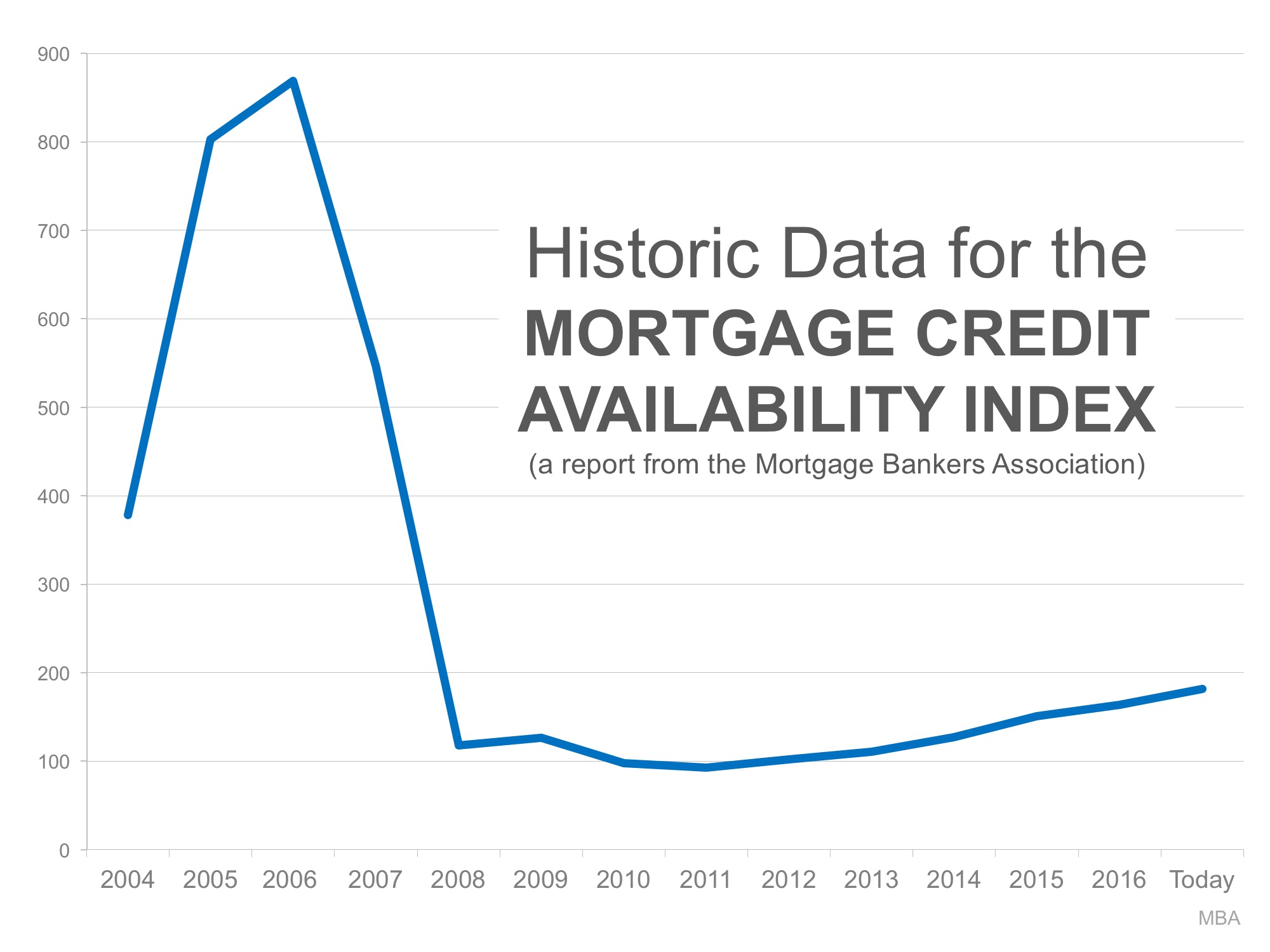

Bubble Alert! Is it Getting Too Easy to Get a Mortgage?

There is little doubt that it is easier to get a home mortgage today than it was last year. The Mortgage Credit Availability Index (MCAI), published by the Mortgage Bankers Association, shows that mortgage credit has become more available in each of the last several years. In fact, in just the last year:

- More buyers are putting less than 20% down to purchase a home

- The average credit score on closed mortgages is lower

- More low-down-payment programs have been introduced

This has some people worrying that we are returning to the lax lending standards which led to the boom and bust that real estate experienced ten years ago. Let’s alleviate some of that concern.

The graph below shows the MCAI going back to the boom years of 2004-2005. The higher the graph line, the easier it was to get a mortgage.

As you can see, lending standards were much more lenient from 2004 to 2007. Though it has gradually become easier to get a mortgage since 2011, we are nowhere near the lenient standards during the boom.

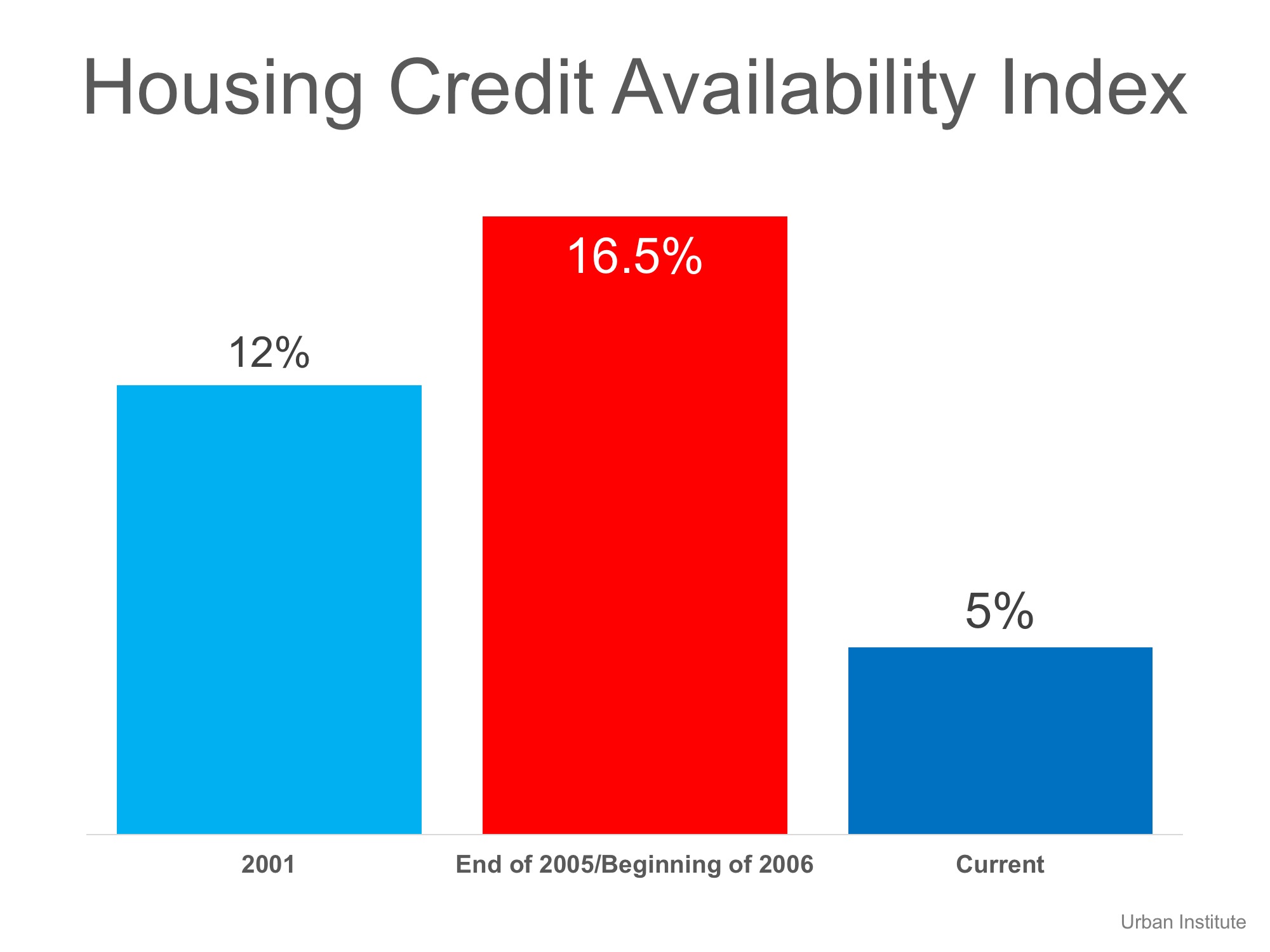

The Urban Institute also publishes a Home Credit Availability Index (HCAI). According to the Institute, the HCAI:

“Measures the percentage of home purchase loans that are likely to default—that is, go unpaid for more than 90 days past their due date. A lower HCAI indicates that lenders are unwilling to tolerate defaults and are imposing tighter lending standards, making it harder to get a loan. A higher HCAI indicates … it is easier to get a loan.”

Here is a graph showing their findings:

Again, today’s lending standards are nowhere near the levels of the boom years. As a matter of fact, they are more stringent than they were even before the boom.

Bottom Line

It is getting easier to gain financing for a home purchase. However, we are not seeing the irresponsible lending that caused the housing crisis.

Want to see how we can help you?

Give us a call and we'll discuss what this development means for you and how you can take advantage of it.

(850) 420-7200

Your Friends Are Crazy Wrong If They're Telling You Not to Buy

The current narrative is that home prices have risen so much so that it is no longer a smart idea to purchase a home. Your family and friends might suggest that buying a home right now (whether a first-time home or a move-up home) makes absolutely no sense from an affordability standpoint. They are wrong!

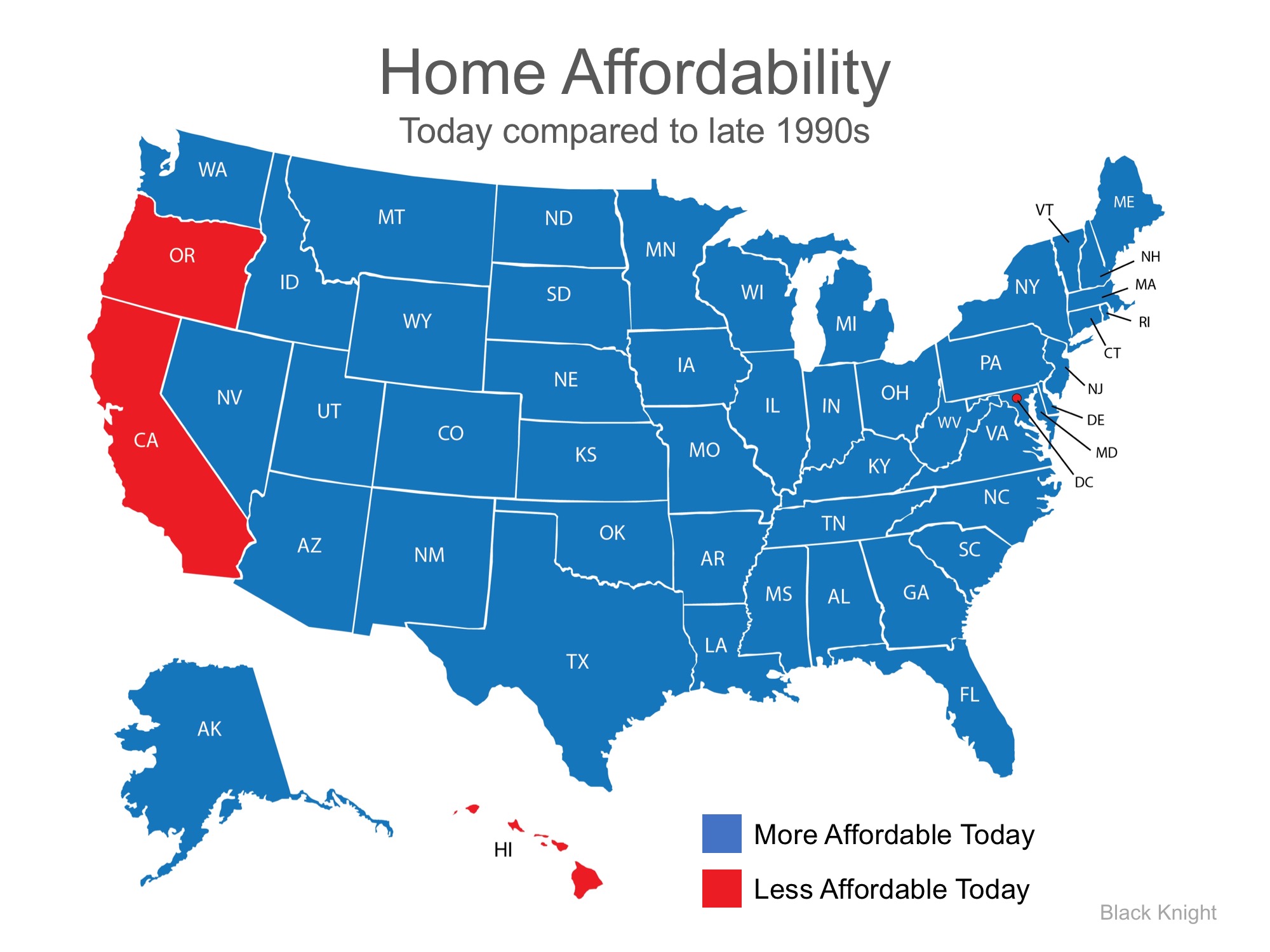

Homes are more affordable right now than at almost any time in our country’s history except for the foreclosure years (2009-2015) when homes sold at major discounts. As an example, below is a graph from the latest Black Knight Mortgage Monitor showing the percentage of median income needed to buy a medium-priced home in the country today in comparison to prior to the housing bubble and bust.

As we can see, the percentage necessary is less now than in those time periods.

The Mortgage Monitor also explains that home affordability is better today than it was in the late 1990s in 47 of 50 states.

Bottom Line

Your friends and family have your best interests at heart. However, when it comes to buying your first home or selling your current house to buy the home of your dreams, let’s get together to discuss what your best move is, now.

Want to see how we can help you?

Give us a call and we'll discuss what this development means for you and how you can take advantage of it.

(850) 420-7200